Distressed property sales in Snohomish County have reached 48% of closed residential transactions, up from 36% for the same time last year.

Bank sale REO property represented 35% and short sales represented 13%.

We are sure that short sales could easily pass the REO numbers if banks could get them closed.

Today there are 735 Pending residential short sale transactions. However, on average, on 72 close per month. That tells us it will take over 10 months just to get those closed, not including new ones that go pending!

The rate of foreclosure filings dropped to their lowest point in nearly 3 years. Is this a sign that the worst is over? We think it is. But what does this really mean? We think that there are many people still struggling to meet their mortgage payments, but banks are working more to keep people in their homes through loan modifications and short sales.

There is also a new milestone in our graphs. Foreclosure "Notices" were lower than "Foreclosures" in the month of September. This is the first time ever that Foreclosures exceed the amount of Foreclosure Notices.

This trend is most likely due to two reasons:

1. Banks are only filing foreclosure notices on homes they are serious about foreclosing on;

2. With the enactment of the new Washington State "Foreclosure Fairness Act", it slows down the process and allows for homeowners to have "face to face" meetings with the bank to work out an agreement before moving forward with foreclosure.

The trend is also showing up in the Snohomish County foreclosure rates as Notices and Foreclosures continue dropping.

Snohomish County foreclosure rates hit their 2nd all time high last month as 339 homes were lost through foreclosure. The all time high was hit in January 2010 at 397 homes. Clearly indicating that homeowners are still struggling financially to make their mortgage payments. We believe that a large percentage of these are strategic defaults as more homeowners walk away from their upside down mortgages.

Click on graph to enlarge.

King County foreclosure rates remain equally high reaching levels seen in the peek of 2010.

An investigativereport issued yesterday by the FDIC regarding Foreclosure practices by large banks including Bank of America, Citibank, JPMorgan Chase, Wells Fargo, GMAC, Ally and third party providers MERS and LPS and others, is missing some important "F" words.

The 12 page document investigating the breakdown during the "robo signing" scandal outlines what they feel were "inadequacies" during the foreclosure process.

They applied a consistent formula and result to each file review that included:

~ Policies and procedures - Rated "Inadequate" ~ Organizational structure and staffing -Rated "Inadequate" ~ Management of third-party service providers - Rated "Inadequate" ~ Compliance with applicable laws - Rated "Inadequate" ~ Loss mitigation - Rated "Inadequate" ~ Critical document control - Rated "Inadequate" ~ Risk Management - Rated "Inadequate"

"Compliance with Applicable Laws" Can someone tell me when breaking the law became an "inadequate" offense rather than a criminal offense?

"Affidavit and Notarization Practices" The investigation found that foreclosure affidavits were signed improperly and failed to conform to State Legal requirements.

The FDIC report misses the first "F" word that needs to be used here. FORGERY.

This was just recently on "60 Minutes" regarding the whole Linda Green story.

Certainly the FDIC watches "60 Minutes" don't they?

Next let's turn to "Documentation Practices":

The investigation found:

"...widespread unsafe or unsound operational practices, including missing documents, execution of documents by unauthorized person, failure to notarize documents in accordance with local laws, inaccurate affidavits..." This is where the FDIC needs to learn the "F" word: FRAUD.

One laughable comment in the report says that Banks need to oversee third party servicers (robo-signers) to:

"...minimize reputation damage..."

What the heck? The FDIC is now giving PR advice? Priceless.

The FDIC evaluates activities conducted through third-party relationships as though the activities were performed by the institution itself."

Does that mean that the institution will be held accountable for third-party actions?

There is no recommendation for penalties or fines. This is a fluff piece with no teeth.

And to top it off it ends with:

"To the extent an institution has a practice of paying law firms, servicers, and employees bonus incentives to process high volumes of foreclosures, the practice should be discontinued"

What the FDIC continues to fail (another "F" word) to understand and question:

WHY THE RUSH TO FORECLOSE?

Answer: To cover up the massive fraud in the loan paperwork from origination.

The rush to foreclose is to white wash or "launder" the lender fraud that can be exposed in the original loan documents.

Home prices are being affected by more than just foreclosures and short sales.

In years past we had a "flipper" market. Investors bought homes that needed updating and it was easy to drop a few thousand dollars into paint and carpet and turn around and sell the home for a good profit.

That was then.

That was when money was easy.

That was when home prices were rising.

Those days are gone. We are now seeing homes in a serious state of neglect like never before. And this is contributing to further errosion of home prices.

These pictures are of a home that just sold in March for $115,000. A pretty cheap price for sure. But just how much money would need to be put into this home to make it habitable again?

And after improvements could the home be sold for a profit?

There is obvious mold issues and one would question whether it should be just torn down.

Because of these types of properties, we forecast that future average and median homes prices will continue to show declines.

But these declines need to be clarified.

1. Average prices will show decline based on deteriorating home conditions.

2. Average prices will drop because most of the home sales are under $300k.

3. Home sales above $500k are scarce and this anomaly pulls down the averages as a whole. There just isn't alot of home buyers looking in this range.

This can skew the data and give false signals that all home values are declining. Which may not be the case.

Homes that are in great condition with good street appeal are selling and selling quickly. This home sold in 17 days for around $315,000.

Home buyers are out there taking advantage of lower home prices and low interest rates. If you're looking for a home that is a "place to live" for years to come, there are plenty of fine homes to choose from.

If you're looking for a "fixer" to flip, be careful. Know what you are getting yourself into. Prepare to spend money on pre-inspections before sealing the deal. There may be many hidden defects that only a professional inspector can determine. Know what your improvement costs are going to be and then add another 20% for unexpected items. Unless it's the right house at the right price, in the right neighborhood we don't advise it. This not the right market for the unexperienced "flipper".

When looking at the charts below we can see that most of the bank owned properties are listed under $300,000.

What this tells us is that banks are NOT foreclosing on upper end homes for the most part.

In Snohomish County there are 414 bank owned properties on the market under $300K but only 58 over $300K.

In King County we have 589 listed under $300K but only 184 over 300K.

CLICK ON GRAPHS TO ENLARGE

So where are all the foreclosures? Most are listed under $300K and most are selling quickly!

When we look at the Absorption Rate Graphs (available in the right hand column under graphs) we see that bank properties are selling almost as quickly as homes are being foreclosed on and they come on the market as REO listings.

We believe that banks are working with most struggling homeowners through loan modifications and approving short sales.

We also believe we are through the worse of times. The market is already showing small signs of improvement and we are on track for a slow but hopefully steady recovery.

The State is putting together legislation to require lenders to offer face to face discussions with distressed homeowners before initiating foreclosure. This new legislation is called the "Foreclosure Fairness Act". In a move to protect distressed homeowners from unnecessary foreclosures, the State of Washington is working on HB1362 . The legislature states that Washington's non-judicial foreclosure process does not have a mechanism for homeowners to access a neutral third party to assist them in a fair and timely way for a work out or mediation regarding their mortgage delinquency. The legislation intends to:

Encourage homeowners to utilize the skills of housing counselors;

Create a framework for homeowners and lenders to communication with each other;

Provide a process for mediation when recommended.

The 3 main parts of the new legislation are:

Opportunity for borrower to request a "face to face" meeting with lender;

Opportunity for mediation with a neutral third party;

$250 filing fee for Lender's Notice of Default.

One important change for the homeowner is that if the homeowner responds to the initial contact by the lender within 30 days, the bill provides the homeowner an additional 60 days to attempt a work out solution with the lender, before a Notice of Default can be filed. During this period the homeowner can request a "face to face meeting" with the lender and at this "meeting", a representative of the lender must be in person. TIP: I would definitely be recording this conversation!

"The subsequent meeting scheduled to assess the borrower's financial ability to repay the debt and discuss options to avoid foreclosure must be in person, unless the requirement to meet in person is waived in writing by the borrower or the borrower's representative"

It is important to note that the borrower must contact an approved housing counselor or attorney to protect their right to mediation, as mediation can only be requested by an approved housing counselor or attorney.

This must be done before issuance of a Notice of Trustee Sale. Once a referral to mediation has been made, a mediation session must occur within 45 days, or can be extended by agreement of all parties. This mediation could be a very powerful and effective tool for homeowners who are having difficulty with loan modification efforts with their lender. WHY? Because at this mediation session the lender must "lay all their cards on the table". Information that may have been withheld from the borrower will be disclosed including:

"A Net Present Value (NPV) of receiving payments pursuant to a modified mortgage loan as compared to the anticipated net recovery following foreclosure."

Sound confusing? You bet. This is a formulated spreadsheet that the lender uses with undisclosed numbers to determine if they will come out ahead better through modification or foreclosure! Also, the lender will not disclose this information to you if you are attempting to modify your loan yourself. Additional documentation must also be provided, such as:

An accurate statement containing the balance of the loan;

Copies of the Note and Deed of Trust;

Proof the Lender is the owner of the Note;

An itemized statement of arrearages;

An itemized list of fees and charges;

Payment history for last 12 month or since default, whichever is longer;

All borrower-related and mortgage-related input data used in any net present value analysis;

An explanation regarding any denial for a loan modification or alternative;

The most recently available appraisal or broker price opinion;

The excerpt of the pooling and servicing agreement AND documentation or a statement detailing the efforts of the beneficiary to obtain a waiver of the pooling and servicing agreement.

The last item is of particular interest. Keep in mind most lenders no longer "own" your mortgage. They are only collecting (servicing) your monthly payment on behalf of the owner of your mortgage, usually a security instrument owned by a pool of investors.

This item requires the lender to disclose any efforts that have made with the investors to try to get them to negotiate a modification on your mortgage, unless there is already language in the agreement that prohibits modifications.

There are many other condition and time lines contained in the bill and we highly encourage homeowners that are suffering financial hardship to seek professional guidance through these issues.

This new bill will result in the State having to set up programs for homeowners that are not now in place. This will include forms, websites, lists of approved housing counselors, attorneys and mediators for the homeowners to access, along with training for all those involved. There is also a $400 cap on the mediation session up to 3 hours. This charge is split 50/50 between the homeowner and lender and must be paid 7 days before mediation. TIP: Mediation is only for owner-occupied residential properties. Do not abandon your home and mortgage if you wish to have access to mediated loan modifications. It may be the best $200.00 a distressed homeowner can spend! Although this legislation is a step in the right direction, the success of the program will be dependant on getting the word out to consumers. I didn't see anywhere in their program regarding any PR or advertising costs.

Also, as is with all rules, there are exceptions. Lenders who file less than 250 foreclosures per year are not held to the mediation rules. If the consumer is not opening their mail from the mortgage lender because "they know it's just another late notice", they may not see the information included that explains these new rules and their rights to request a "face to face" meetings and mediation possibilities.

Second, I feel that the consumer is in need of a "Home Owner's Bill of Rights".

How is it that someone who makes timely mortgage payments for 10-20 years and suffers a temporary financial hardship or loss of income can lose their home to foreclosure in 120 days? There is something fundamentally wrong with this scenario. We are well versed on foreclosures, short sales and loan modifications. If you or anyone you know need some help or direction, please call us. We are here to help and there is never any charge or Fee. Please use us as a resource to help during these difficult times.

AND never pay anyone for a loan modification - If someone wants to charge you a fee up front - run in the opposite direction because it's a scam.

Disclosure: This bill has not been finalized and is subject to change. Nothing in this article should be construed as legal advice and homeowners are always encouraged to consult with an attorney for legal interpretation of the bill, as there are many other requirements and timelines that must be met that are not covered in this article. The full House Bill 1362 can be read here: HB1362

Have you been house-hunting and having a hard time finding that great buy?

If you've been looking at Bank owned properties in the $400,000 - $500,000 price range in King County, have you found there are few to choose from? Did you know there are only 31?

The same price range in Snohomish County will offer you a whopping 18.

You might say "wait, but where are all the foreclosures we read about in the media?"

Well, they are out there, but unless you are looking for a "fixer upper" under $200,000 the choices will be few.

Click on graphs to enlarge.

When we look at the current inventory of distressed properties in King County, we have found that most fall under $300,000. As a matter of fact, 76% of all the active listings under $200k are distressed property listings which include short sales.

Distressed properties are defined as bank owned (REO) properties and short sales (home owners who owe more on their mortgage than the current listing price).

Now we're not saying you can't find that diamond in the rough, but if you're looking to buy a great bank owned property, you're mostly likely just going to find the "rough". But there are some definate bargins to be found!

Checking bank owned homes in Seattle under $300,000 there are only 126 out of 586 in King County. That means that a majority of them are in outlining areas such as Renton & Federal Way. Here's a sampling of bank owned inventory under $300K by area:

White Center Area = 31

West Seattle =40

South Seattle/Rainier = 34

Beacon Hill = 8

North of Lake Union = 11

Even with all the headlines about foreclosures these days, we are finding that the banks are changing their tune regarding foreclosures. We know there are many who are struggling to meet their mortgage payments, but we also see banks pushing through more home loan modifications and starting to approve short sales quicker.

Short sale properties can be a good buy, but few are willing to wait the 4 months it takes to get an offer approved. So until that process is streamlined by the banks, we don't see a rush to short sale purchases.

For 2010 we see that in King County 15% of closed sales were bank owned properties and 10% were short sales. So keep in mind that 75% of all home sales for 2010 were non-distressed home transactions. See graphs in right hand column for distressed properties sales for 2010.

We continue to watch the trends, stay tuned for monthly updated charts on foreclosure and short sale stats.

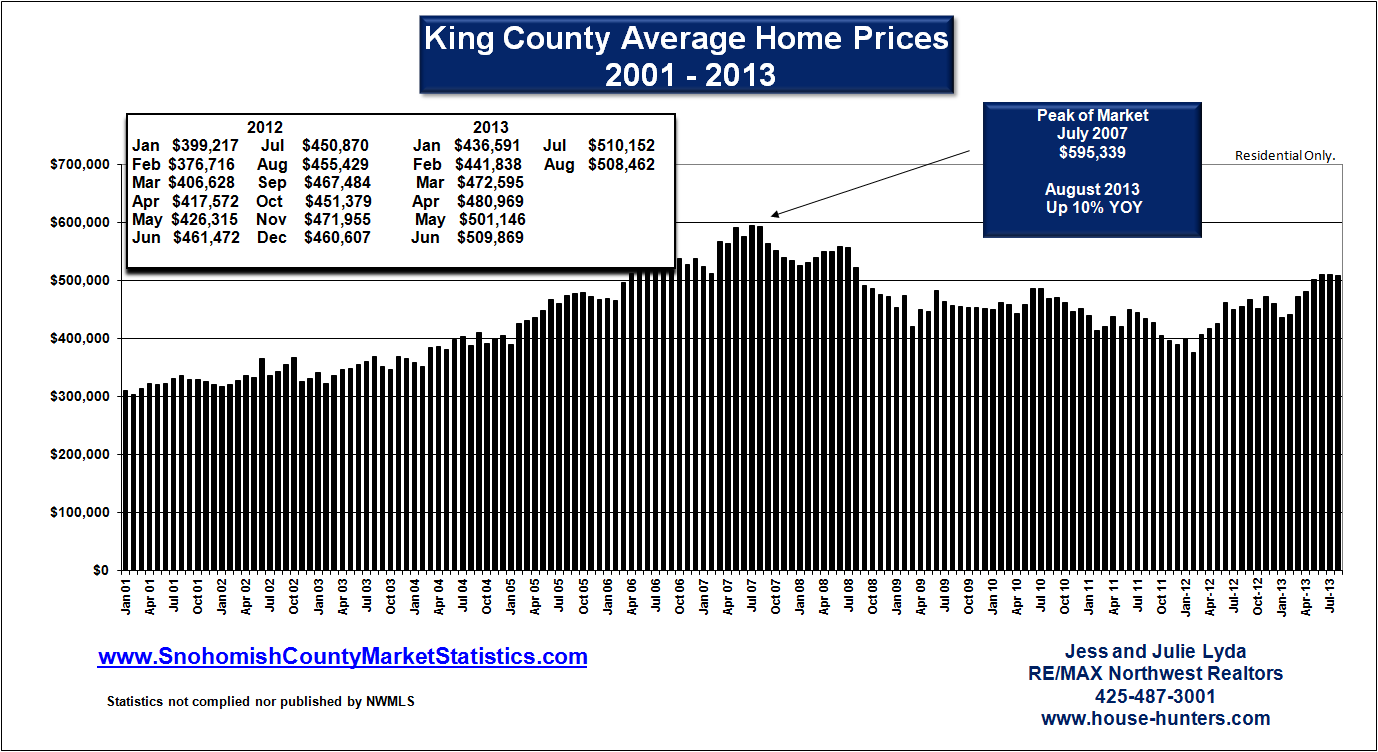

King County home prices posted their first gains in three years. After three years of continued decline, King County home prices may have finally reached their bottom. December 2010 ended the year with a surprise jump in home sales along with home prices. Many communities in King County posted year over year price gains, while others are still showing losses.

This reinforces the popular tag line "location, location, location" .

When checking the individual communities on the City Charts in the right hand column, we see that several cities posted positive price gains:

Bellevue Kirkland Redmond Edmonds Lake Forest Park Woodinville

We track only north and east of Seattle communities, there may be gains in other areas.

An increase in average home prices doesn't necessarily mean homes have risen in value, but rather higher priced homes have been selling which brings up the overall average. This is important to keep in mind, as we still see downward pressure on home prices overall.

Rising inventories of distressed home sales and foreclosures will certainly keep the pressure on prices, but the tide could be changing. This is also a clear indication that prices are no longer "falling off the cliff" and we are reaching a level of stabilization.

Certain economic conditions play a role in our local home prices, so while we still have lackluster employment numbers the market is most likely to remain flat until conditions improve.

Does that mean it is a good time to buy a home? If we take into consideration interest rates being at all time lows, it could be. There are many reasons people purchase homes. A place to live, an investment property, or a money maker.

For most home owners, buying a home was always a long term investment. That's what went wrong during the housing bubble. The days when one talked about paying off their mortgage so they could live rent free. Not irrational exuberance in sucking out equity to buy more things.

Homeowners make a community. They have long term visions associated with their home. They get involved in community and neighborhood organizations. Communities with higher home ownership have better educational performance and lower crime rates.

Still, while financial advantages shouldn't be the first and only thing to consider when we think about owning a home, it would be foolish to discount these benefits altogether. The opportunity to take advantage of tax deductions for mortgage interest and property taxes or the ability to benefit from the capital-gains exclusion on the sale of a home up to $500,000.

So there are other factors to consider when deciding to purchase a home other than sales price. Interest rates, tax benefits, community benefits, and the emotional benefits.

So is the market finally reaching a bottom? We will only be able to tell when we see price increases over a longer period of time. However, we see the market is opening up some great buying opportunities for some who are taking advantage of them now.

Snohomish County foreclosure rates rose 50% YOY from 2009 to 2010. Looking at the chart we see the last peak in foreclosure rates was in 2003 following a 3 year rise. Hopefully the trend repeats and 2010 will be the peak with a leveling off in 2011.

Snohomish County foreclosures took a breather for the holidays. December's numbers dipped to 119 from 209 in November. The last two years showed the same trend and we fully expect foreclosures to raise during the next few months.

The worst month so far has been January 2010 followed by August, 2010 and October 2010. The next few months' numbers will give us a better idea of what the trend will be for the year.

Click on graph to enlarge.

Click on graph to enlarge.

{kind=link}